How to Read a P&L Statement

A confirmation email has been sent to your email.

Your financial statements are a key tool in managing your business. They give you the information you need to understand your business’s health, and make accurate projections about its future. Today, we’re taking a look at how to read a Profit & Loss (P&L) Statement.

What is a Profit & Loss Statement?

The Profit & Loss statement, also called an income statement, shows you your revenue and expenses over a certain period of time. The revenue section covers how much money your business brought in for that period, and subtracts the cost of creating your products to show your gross profitability. The expenses section covers how much money you spent over the period, and breaks out different categories of spending to show how much you spent in each area. It also subtracts your expenses from your gross profit, to determine if your business is operating at an overall profit or a loss.

Along with your balance sheet and statement of cash flows, the P&L statement helps you build a complete picture of your company’s financial position.

P&L Statement vs. Balance Sheet

A common question we get around P&L statements is, how is it different from a balance sheet? They both show you the amount of money you have and the amount you’re spending, right? Not quite. While both the balance sheet and the income statement give you information about money coming in or going out, the key difference is time.

Your balance sheet shows your business’s assets and liabilities for a particular point in time: for example, the last day of the previous month. Reading your balance sheet will tell you that on that particular date, your company owned a certain amount of money in assets (such as cash in the bank, fixed assets like office equipment, expected income in accounts receivable), and owed a certain amount in liabilities (such as payroll, credit card charges, and rent). A balance sheet created a week later might have different numbers – for example, if the credit card charges had been paid off, or a new sale was made. It’s a snapshot of what your business looked like on that date.

Your income statement, on the other hand, shows your revenue and expenses over the entire period (which might be a month, quarter, year, etc). Instead of listing how much was in the bank on a certain date, how much was in AR, etc, the income sheet will list how much revenue you made in that time, and how much your gross profit was for that period. It will also break out your expense categories, and how much you spend in each one.

In short: the balance sheet is a snapshot of what your business looks like on a specific date, while the P&L statement shows how your business changed over a specific time period.

What is a P&L Statement Used For?

The P&L statement is useful for examining trends in your business, and understanding where you’re bringing in money (and where you’re losing it):

- Are you making a gross profit (i.e., are you making enough in revenue to cover the cost of creating your product?)

- If you have more than one revenue stream, how are they performing against each other?

- Where are you spending most of your money?

- Are there any big expenses categories you might be able to lower?

Your income statement can surface questions you should ask, and potential problem spots to investigate.

Besides flagging possible issues, the P&L statement can also highlight opportunities for growth. If a particular area of your business is bringing in a lot of revenue, you might consider investing more resources in that area to help it expand. Conversely, if there are any struggling products or business lines, you can consider how to improve them – or decide they just aren’t a good fit for your business.

How to Read a P&L Statement

The P&L statement shows your income, COGS, gross profit, expenses, net operating income, and total net income. Let’s look at an example.

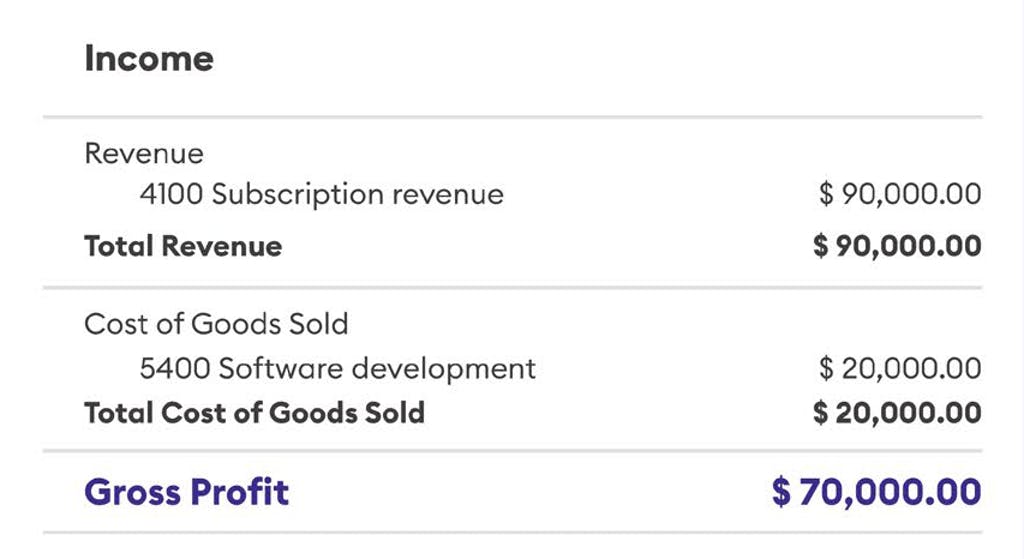

The first part of the P&L statement covers income, COGS, and gross profit. Above, we see that our example company made $90,000 in subscription revenue over the period covered by this statement. This is where all the money you bring in from sales will be listed, broken out by source. If your company sells both subscriptions and physical products, for instance, those sales will be listed as separate types of revenue.

Beneath the total revenue, we have the Cost of Goods Sold (COGS). This is how much it costs the company to create the product or service it’s selling. Here, we see that our example company spent $20,000 in software development to be able to deliver their product.

To get gross profit, we subtract the COGS from the total revenue. This tells us that, before other expenses are factored in, our example company made a profit of $70,000 over the period.

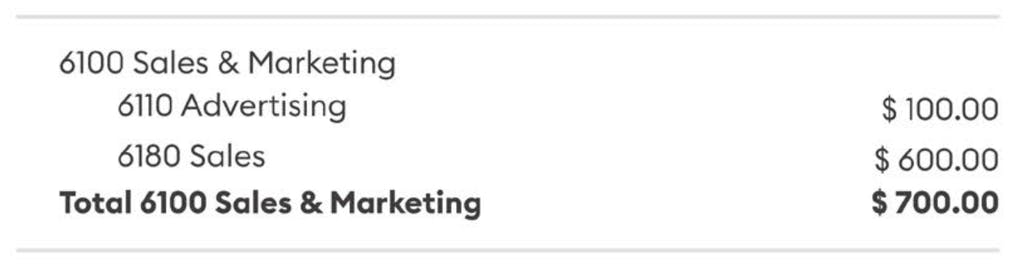

After the revenue section, we come to the expenses. These are broken out into categories and sub-categories, to give you a better picture of what you’re spending money on. Here, we see the example company spent $700 total on sales and marketing, with $100 going towards ads and $600 going towards sales costs (commission, etc).

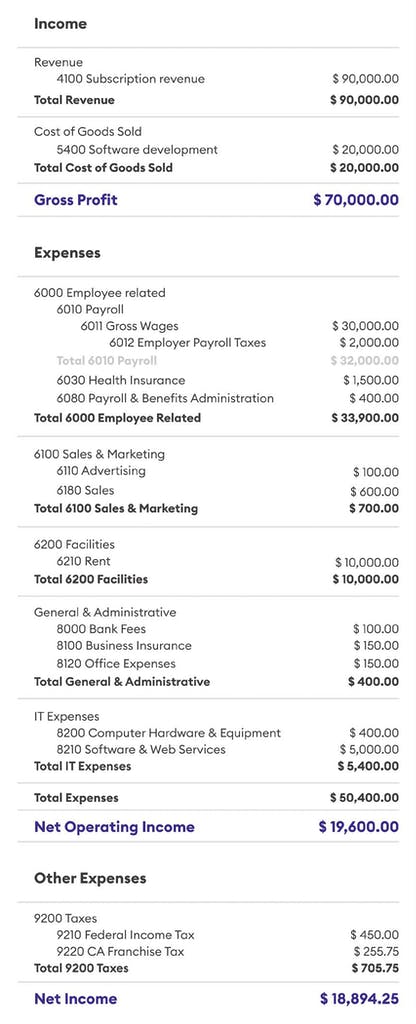

For some categories, the expenses may be broken down even further. Here we look at an example for employee-related expenses – which for most companies will be the largest expense category on their statement. In the example above, we see that wages are only part of the employee costs. In addition to the gross wages, our example company paid $2,000 for payroll taxes, $1,500 for health insurance costs and $400 related to administering benefits. In total, the company paid $33,900 in costs related to their employees over the statement period.

The income statement will list all of your expenses across all categories, including facilities costs, general & administrative costs, IT costs, and anything else that the company paid for. At the bottom of the operating expense section, these are added up to get the total expense amount. This is then subtracted from the gross profit, to get the net operating income.

Net operating income is one of the most important lines on the P&L statement, because it shows what’s left over after all your expenses are paid. If the number is positive, it means your business is profitable. If it’s negative, however, it means that your business is spending more than it brings in, and you’re burning capital just to stay in business. This is normal for companies like startups, of course, but even if you expect to operate at a loss, you’ll still want to keep an eye on just how much you’re burning.

For our example company, all expenses in all categories add up to $50,400. If you’ll recall, our example company had a gross profit of $70,000. $70,000 – $50,400 = $19,600, which is their net operating income. Because this number is positive, it means our example company is profitable.

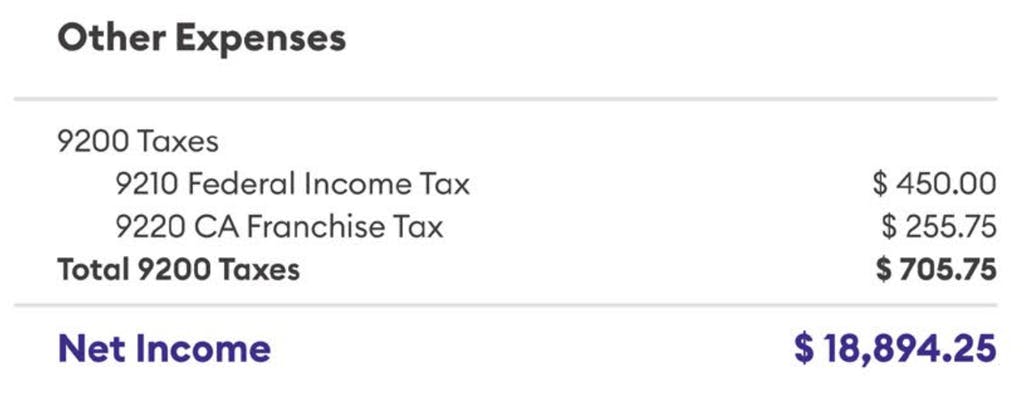

Finally, any non-operating expenses are listed. In this case, taxes – not related to running the business, but still an important expense to be paid. The example company paid $705.75 in taxes, and when we subtract that amount from the net operating income, we get the total net income for the example company: $18,894.25.

Here’s what the whole P&L statement looks like when you put it together:

The profit and loss statement is a crucial tool in managing your business’s money, and knowing how to read one is vital to getting the information you need to run your company. With a solid grasp of how your company is trending and which areas to focus on, you’ll be able to make more accurate financial projections, and better recognize your opportunities to grow.

Still not sure how to approach your P&L statement – or what to do with the information it gives you? Pilot’s bookkeeping and CFO services are always here to help.